Can my parent PLUS loan be forgiven?

Can my parent PLUS loan be forgiven?

A federal parent PLUS loan may be eligible for forgiveness through an income-contingent repayment plan or through the Public Service Loan Forgiveness program. In most cases, a parent borrower will take out a PLUS loan once their child reaches their federal student loan limits to cover the remaining costs.

What happens if I don’t pay my parent PLUS loan?

While your parent PLUS loans are in default, the government can garnish your wages and take your tax refunds and Social Security checks, among other consequences. Defaulted loans also aren’t eligible for different repayment plans, or deferment or forbearance.

How do I consolidate a parent PLUS loan?

Step 1: Apply for a Direct Consolidation Loan through StudentLoans.gov. Step 2: Talk to your loan servicer and choose ICR. Step 3: Make payments on time for 25 years to get your loans forgiven. Pay any potential tax bills related to your loan forgiveness.

Is spouse responsible for parent PLUS loan?

Only the parent borrower is required to pay back a Parent PLUS Loan, as only the parent signed the master promissory note for the Parent PLUS Loan. The student is not responsible for repaying a Parent PLUS Loan.

How do I consolidate my parent PLUS loans?

How long do you have to pay back parent PLUS loans?

You will be repaying the debt for 10-25 years regardless of the option you select. Choose a parent PLUS Loan repayment option that works for you and your family and stay the course. Parent PLUS loans do not have prepayment penalties, You can pay off the loans sooner than 10 years by making extra payments on the debt.

How do you pay off student loans?

How to Pay Off Student Loans Fast

- Make extra payments the right way.

- Refinance if you have good credit and a steady job.

- Enroll in autopay.

- Make biweekly payments.

- Pay off capitalized interest.

- Stick to the standard repayment plan.

- Use ‘found’ money.

What happens if I never pay my student loans?

Let your lender know if you may have problems repaying your student loan. Failing to pay your student loan within 90 days classifies the debt as delinquent, which means your credit rating will take a hit. After 270 days, the student loan is in default and may then be transferred to a collection agency to recover.

Can you go to jail over student loans?

Can You Go to Jail for Not Paying Student Loan Debt? You can’t be arrested or sentenced to time behind bars for not paying student loan debt because student loans are considered “civil” debts. This type of debt includes credit card debt and medical bills, and can’t result in an arrest or jail sentence.

What’s the fastest way to pay off Parent PLUS loans?

If you don’t qualify for refinancing or loan forgiveness, making payments on the standard, 10-year federal repayment plan will pay off parent PLUS loans the fastest and save you the most money. To become debt-free even quicker, make extra student loan payments toward your principal balance.

Who is responsible for repaying the Parent PLUS loan?

Well, the burden of repayment falls squarely on the parent borrower, since the loan was borrowed in their name. But even if the student is not responsible for paying the parent PLUS loan, they might want to pitch in with repayment or even refinance the parent loan in their own name.

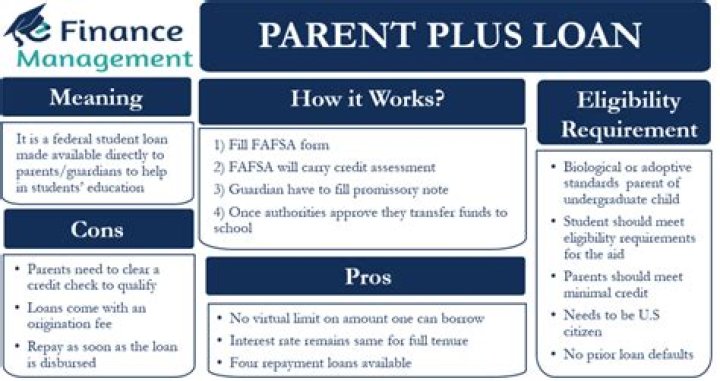

How do I apply for a Parent PLUS loan for my child?

Contact the financial aid office at the school your child is planning to attend for details regarding the process at that school. If you’re taking out parent PLUS loans for more than one child, you’ll need to sign separate Direct PLUS Loan MPNs for the loans you receive for each child.

How do I switch from Parent PLUS to Income-Contingent Repayment?

To be eligible, you must first consolidate your parent PLUS loans. Switch to Income-Contingent Repayment only if you can’t afford payments on the standard 10-year federal repayment plan. On Income-Contingent Repayment, you’ll pay more in interest and you’ll be required to pay income tax on any amount forgiven.